The Complete Under-25 Guide (US Edition)

So you found a great deal on a used Honda Civic. Clean interior, decent miles, and a price that actually fits your budget.

Then you noticed two words in the listing: rebuilt title.

Now your insurance search is turning into a nightmare. Sound familiar?

You are not alone. Thousands of Gen Z drivers across the US face this exact situation every year.

The good news? Insuring a rebuilt-title Civic under 25 is absolutely possible. You just need to know which companies to call, what questions to ask, and what traps to avoid.

This guide covers everything: the best insurers, the step-by-step process, the real financial risks, and the FAQs your dealership definitely will not answer.

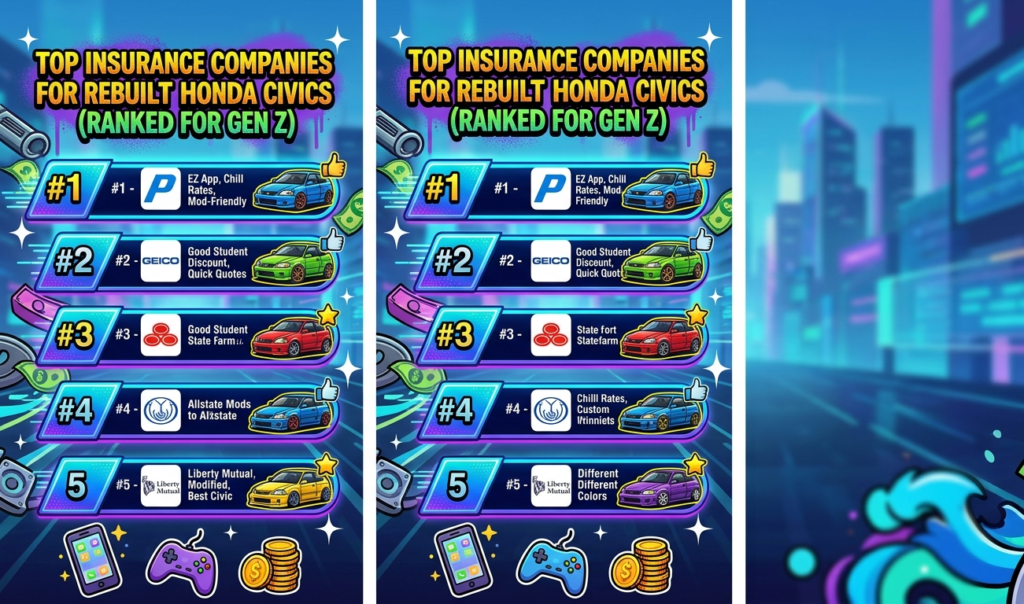

Top Insurance Companies for Rebuilt Honda Civics (Ranked for Gen Z)

Not every insurer will touch a rebuilt title.

And the ones that do often charge significantly more when you are under 25.

Here is a straight-up ranked breakdown so you know exactly where to start your search.

| Insurer | Rebuilt Title? | Under 25 Friendly? | Full Coverage? | Best For |

| Progressive | Yes | Yes | Often available | First-time buyers |

| State Farm | Yes | Yes | Case by case | Student discounts |

| GEICO | Varies | Harder | Rarely | Clean-title drivers |

| Liberty Mutual | Varies | Harder | Rarely | Older drivers |

| Dairyland | Yes | Yes | Limited | High-risk drivers |

Progressive: Best Overall for Rebuilt Titles Under 25

Progressive is widely considered the most rebuilt-title-friendly major insurer in the US.

They actively write policies on salvage and rebuilt vehicles and do not automatically shut the door on young drivers.

Here is why they lead the pack:

- They use a usage-based rating model called the Snapshot program. This means a clean driving record can actually offset some of the under-25 surcharge.

- They are more likely to offer Comprehensive and Collision coverage on a rebuilt Civic than most competitors. This depends on the inspection results, but it is on the table.

- Their online tool gives preliminary quotes. For rebuilt titles though, always follow up by phone. The difference in what an agent can offer versus what the website shows can be significant.

Real-World Example: If you bought a 2020 Honda Civic LX for $12,000 with a rebuilt title in Texas, Progressive may still offer you liability plus comprehensive for around $180 to $230 per month as a 22-year-old. That is roughly 30 to 40 percent more than a clean-title equivalent, but it is still insurable.

State Farm: Best for Students and Good Drivers

State Farm is the other major player worth calling first.

Their agents have more discretion than automated systems. They also offer one of the most valuable discounts available for young drivers: the Good Student Discount.

- Maintain a 3.0 GPA or higher? State Farm can knock 10 to 25 percent off your premium. That goes a long way against the under-25 surcharge.

- State Farm agents vary by location. One agent might decline your rebuilt Civic while another in the next county approves it. Always try multiple agents before giving up.

- They are generally better for Civic with light damage histories, like a fender-bender total loss, compared to vehicles with severe structural damage in their past.

Why GEICO and Liberty Mutual Are Harder for Under-25s with Branded Titles

GEICO and Liberty Mutual are not bad insurers in general.

But they are not ideal if you are young and driving a rebuilt-title car. Here is why:

- GEICO’s underwriting algorithm is heavily automated. A rebuilt title combined with being under 25 and having limited credit history often results in an automatic decline or a liability-only quote at a steep price. There is very little room for human override.

- Liberty Mutual tends to be more conservative with non-standard vehicles. They may offer a quote, but Comprehensive and Collision coverage is rarely on the table for rebuilt cars driven by young people.

- Neither company offers strong pathways to appeal a denial. You would need to go through an independent agent, which adds complexity and time.

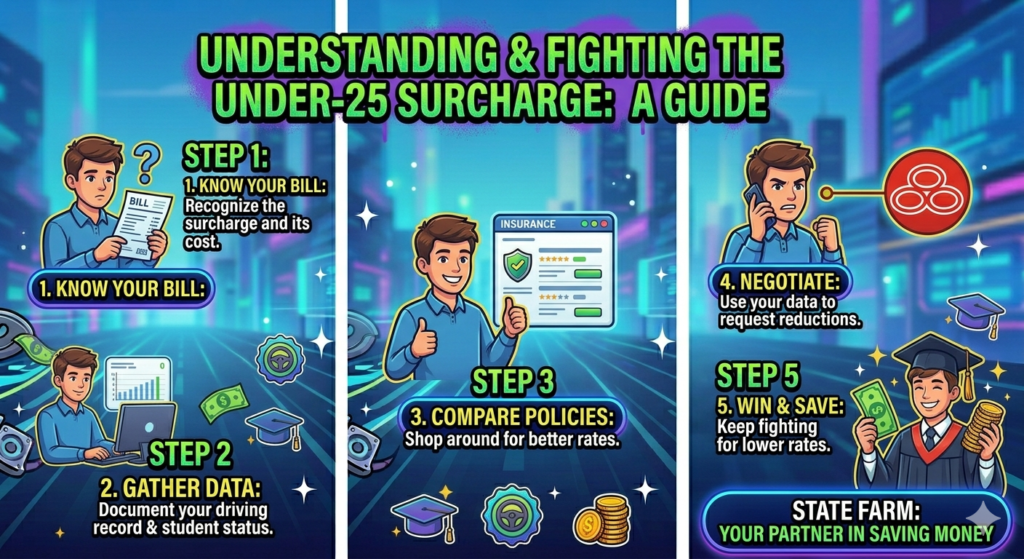

Understanding the Under-25 Surcharge and How to Fight It

Here is the hard truth: being under 25 is statistically the biggest risk factor in car insurance.

Insurers add what is called an age surcharge. This is a premium bump that can add 50 to 100 percent to your base rate compared to a 30-year-old with the same car.

Layer a rebuilt title on top of that and you are looking at a compounded risk profile.

The good news is there are legitimate ways to push that number back down:

- Good Student Discount: Maintain a 3.0 GPA and ask about this discount at every insurer you call.

- Defensive Driving Course: A state-approved course costs $30 to $80 and can cut your premium by 5 to 15 percent.

- Stay on a Parent’s Policy: If your parents have a clean record, adding you and the rebuilt Civic to their existing policy is often cheaper than a standalone policy.

- Higher Deductible: Choosing a $1,000 deductible instead of $500 lowers your monthly premium. Only do this if you have the cash savings to cover it.

- Usage-Based Insurance: Programs like Progressive Snapshot or State Farm Drive Safe and Save track your driving habits. Safe drivers under 25 can earn back 10 to 30 percent in discounts.

| ⚡ Pro Tip: Stack Your DiscountsThe Good Student Discount and a Defensive Driving Course discount can often be combined.On a $200 per month premium, stacking a 15 percent student discount and a 10 percent safe driver course discount saves you $50 per month.That is $600 per year. Do not leave that on the table. |

Step-by-Step Process to Get Covered

| ⚡ Pro Tip: Call at Least 3 to 5 AgentsDo not stop at one call.Contact Progressive, State Farm, and at least one independent agent who represents multiple companies.Independent agents can shop your rebuilt-title profile across 10 to 15 insurers simultaneously.They often find options that big direct carriers and comparison sites completely miss. |

Insuring a rebuilt-title Civic is not like clicking through a five-minute quote form.

You need to do your homework first and do it in the right order.

Skip a step and you risk being denied, overpaying, or discovering after an accident that your policy does not cover what you thought it did.

Step 1: Run a VIN Check (NICB and Carfax)

Before you even call an insurer, run a full Vehicle Identification Number (VIN) check.

You need at minimum two reports:

- NICB VINCheck (free at nicb.org): This checks whether the car was ever reported stolen or declared a total loss. It takes about 30 seconds.

- Carfax or AutoCheck ($40 to $50): This shows the full damage and repair history, previous title brands across all 50 states, and the number of previous owners.

Why does this matter for insurance?

Because insurers will pull this data themselves. If the history reveals undisclosed damage, like frame damage the seller never mentioned, they can void your policy or deny a claim after an accident.

Know exactly what you are buying before you sign anything.

What to Look For: A Rebuilt or Reconstructed status on the report is manageable and workable.

Red Flags: Flood damage or structural damage listed on the Carfax is a serious warning sign. Some insurers will not write a policy on those vehicles at all.

Step 2: Get a Certified Safety Inspection (Non-Negotiable)

| State Inspection Requirements VaryStates like California, Texas, and Florida have formal rebuilt-title inspection programs with specific requirements.States like Montana have more relaxed rules.Always check your state’s DMV website for exact rules before purchasing a rebuilt-title vehicle. |

A rebuilt title means the car was previously declared a total loss and then repaired.

To legally drive it in most US states, it needs to pass a state-certified rebuilt title inspection.

But even in states that do not require it, getting an independent inspection is non-negotiable for insurance purposes.

Here is why: most insurers offering coverage on rebuilt Civics will either require an inspection report or assume the worst without one. A certified inspection from an ASE-certified mechanic or state inspection station proves the car is roadworthy and properly repaired.

- Cost: $100 to $300 depending on your state and mechanic.

- What gets checked: Brakes, frame integrity, airbags, electrical systems, and VIN verification.

- Pro move: Ask for a written report you can email directly to insurance agents. This becomes a negotiating tool.

Step 3: Get a Professional Appraisal (Especially for Si and Type R Trims)

If you are insuring a base Civic LX or EX, a standard ACV estimate from an insurer might be reasonably close to real market value.

But if you bought a Civic Si or Type R with a rebuilt title, you need a professional written appraisal. Here is why:

The Si and Type R have significantly higher stock values plus aftermarket parts that standard insurer databases consistently undervalue.

Without an appraisal, your insurer might calculate an ACV of $18,000 on a Civic Type R you paid $28,000 for after modifications. That leaves you with a $10,000 gap if the car is ever totaled.

- Find an ASE-certified appraiser or use a specialty car appraisal service that handles modified or performance vehicles.

- Get the appraisal in writing with photos, current market comparisons, and part-by-part documentation.

- Submit this to your insurer when requesting Agreed Value or higher coverage limits.

Real-World Example: A 22-year-old in Ohio bought a 2019 Civic Type R FK8 with a rebuilt title for $28,500. Without an appraisal, State Farm quoted an ACV of $22,000. With a professional appraisal documenting current FK8 market rates, he secured a $27,000 coverage limit. That $5,000 difference could be everything in a total loss situation.

Step 4: The Call vs. Click Rule for Rebuilt Titles

Here is something most online insurance guides will not tell you:

Online quote tools are designed for standard, clean-title vehicles.

If you plug in a rebuilt title on a comparison site or go straight to GEICO.com, you will often get one of three bad outcomes:

- An automatic denial with no explanation.

- A liability-only quote with no option for full coverage.

- A quote that does not reflect what an agent could actually offer you in person.

The rule is simple: for rebuilt titles, always call a licensed insurance agent directly.

Here is what calling actually gets you:

- Human underwriting override: Agents can submit your file for manual review, bypassing automated denials that the website would give you instantly.

- Bundle negotiation: An agent can check whether adding renters insurance or another policy unlocks better rates on your rebuilt Civic policy.

- State-specific knowledge: Some states have programs or surplus lines insurers that online comparison tools simply do not surface.

- Advocacy for your inspection report: You can email your certified safety inspection directly to the agent and use it as real evidence that the car is safe.

Critical Risks: What the Dealership Will Not Tell You

| ⚡ Pro Tip: Run the ACV Math Before You BuyBefore purchasing, ask an insurer to estimate the ACV on that specific vehicle.Compare it to your purchase price and expected loan payoff amount.If the ACV is lower than what you would owe after a total loss, either walk away or renegotiate the purchase price down. |

A rebuilt-title Civic can be a smart financial move.

But only if you go in knowing the full picture.

Here are the risks that dealerships and private sellers rarely volunteer on their own.

ACV (Actual Cash Value): The Payout You Are Not Expecting

ACV stands for Actual Cash Value. This is what your insurance company will pay if your car is totaled.

And here is the brutal reality of rebuilt titles: your ACV is already lower than a clean-title equivalent before any accident even happens.

Most insurance companies reduce the ACV of rebuilt-title vehicles by 20 to 40 percent compared to the same car with a clean title.

What does that mean in real dollars?

- If you bought a 2020 Civic LX for $12,000 with a rebuilt title, do not expect a $15,000 payout if someone hits you. A realistic ACV might be $8,500 to $10,000. That could be less than what you actually paid for the car.

- If you still owe money on a loan for the car, you could end up underwater. That means owing more to the lender than the insurance company will pay out.

Liability vs. Full Coverage: The Coverage Brick Wall

Many drivers under 25 with rebuilt-title vehicles discover a frustrating reality after purchase.

They can only get liability coverage, not Comprehensive and Collision.

Here is the difference:

Liability covers damage you cause to other people and their property. Comprehensive and Collision cover damage to your own car. For a rebuilt Civic, this gap matters enormously.

- If someone rear-ends you and totals your car and you only have liability coverage, you are left with a destroyed car. Your only option would be whatever you can pursue through their insurer or in small claims court.

- Full coverage is available for rebuilt titles, but it is harder to get when you are under 25. It usually requires a recent and documented safety inspection.

- Progressive and State Farm are your best bets for full coverage on a rebuilt Civic, but even they may decline based on the severity of the original damage.

| The Coverage Reality CheckAsk every insurer this exact question upfront:”Will you offer Comprehensive and Collision coverage on a rebuilt-title Honda Civic?”Do not assume. Get a clear answer before you commit to any policy. |

Resale Value: The 20 to 40 Percent Penalty You Will Pay Later

This is not strictly an insurance issue, but it connects directly to your financial planning.

A rebuilt title permanently reduces the resale value of your Civic by 20 to 40 percent compared to a clean-title equivalent.

Here is what that looks like in practice:

That 2020 Civic LX you bought for $12,000 with a rebuilt title? In two years, a clean-title version might sell for $14,000. Yours might fetch $9,000 to $10,500.

This affects your ACV calculation, your ability to trade up, and your overall financial position if you financed the purchase.

| ⚡ Pro Tip: Rebuilt Titles Are Best for Long-Term OwnersA rebuilt-title Civic makes the most financial sense if you plan to drive it for five or more years and pay with cash or a very small loan.The value drop hurts the most on financed vehicles with short ownership timelines.If you are planning to sell or trade it within 18 months, the math rarely works in your favor. |

FAQs: Rebuilt Civic Insurance Under 25

These questions come directly from Reddit threads in r/personalfinance and r/Insurance as well as Quora discussions where young drivers are figuring this out in real time.

Q1: Can I get a car loan for a rebuilt Civic under 25?

Technically yes, but it is genuinely difficult.

Most major banks including Chase, Wells Fargo, and Bank of America will not finance rebuilt-title vehicles. Your best options are credit unions, which have more flexible underwriting, or in-house dealer financing.

Expect a higher interest rate, typically 2 to 4 percent above clean-title rates, and potentially a lower loan-to-value ratio. That means you may need a larger down payment.

Some lenders cap loans at 80 to 90 percent of ACV. On a rebuilt title, that ACV is already lower than the purchase price, so you could be expected to cover a significant gap out of pocket.

Q2: Will my parents’ insurance go up if I add a rebuilt car to their policy?

Yes, almost certainly. But potentially less than you would expect.

Adding a rebuilt vehicle to an existing multi-car policy is almost always cheaper than a standalone policy for a young driver. Your parents’ premium will go up for the rebuilt vehicle and for adding you as a driver if you are not already listed.

The key question is whether their insurer even accepts rebuilt titles. Call and ask before assuming it is an option. Progressive and State Farm are again the safest bets for this.

Q3: Is Gap Insurance available for rebuilt titles?

The short answer is usually no.

Gap insurance covers the difference between what you owe on a loan and what insurance pays out in a total loss situation. For rebuilt-title vehicles, gap insurance is almost universally unavailable.

The frustrating irony is that rebuilt-title vehicles are exactly where you would need gap insurance the most, since the ACV is already lower than what you likely paid.

If you are financing a rebuilt Civic, you are taking on the full gap risk yourself. This is another strong argument for paying cash or keeping the loan amount well below the likely ACV.

Q4: Which US states are strictest with rebuilt Civic inspections?

California, New York, Texas, and Pennsylvania have the most rigorous rebuilt title inspection requirements.

California requires a formal Brake and Light Inspection plus a VIN verification by the California Highway Patrol before a rebuilt title is issued.

New York requires a state police inspection. Texas has a two-step process through the TxDMV.

On the more lenient end, states like Montana, North Dakota, and Vermont have lighter requirements. However, this can work against you if you later move to a stricter state and need to re-register the vehicle there.

Q5: What if my rebuilt Civic gets totaled again?

If a rebuilt-title vehicle is declared a total loss a second time, the title reverts back to salvage status.

You would need to go through the full rebuilt title process again: repairs, a certified inspection, and retitling through your state’s DMV.

Most insurers that were already cautious about insuring a first-time rebuilt title will not write a policy on a twice-salvaged vehicle at all.

This is an important risk to factor into your coverage decisions and how much protection you want to carry.

Q6: Are there insurers that specialize in rebuilt or salvage titles?

Yes, and they are worth knowing about.

Beyond Progressive and State Farm, specialty insurers like Dairyland, Bristol West, and National General work specifically with non-standard vehicle histories and high-risk driver profiles.

They are not the cheapest option, but they are more willing to write full coverage on rebuilt titles than most mainstream insurers.

The fastest way to access these specialty markets is through an independent insurance broker. A broker can shop your profile across multiple specialty insurers at once. That is something direct insurers and comparison websites simply cannot do for you.

| Bottom Line for Under-25 Rebuilt Civic OwnersStart with Progressive and State Farm.Run your VIN check and get a certified inspection before you call anyone.If you are a student with a solid GPA, always ask about the Good Student Discount.For rebuilt titles, the phone is your most powerful tool. Skip the online quote forms and talk to a human agent who can actually fight for your coverage. |

For informational purposes only. Always verify coverage details with a licensed insurance agent in your state.